Retirement planning isn’t just about reaching a number.

As retirement approaches, financial decisions often become more complex.

Questions around income, taxes, healthcare, market volatility, and legacy planning can all begin to overlap at the same time.

Our role is to help bring clarity to those decisions so you can move into retirement with greater confidence and direction.

Whether you’re 5 years away or already retired, we help coordinate the financial pieces into a plan designed around your life—not just your portfolio.

Planning for the Risks Retirement Can Bring

Why Timing Matters in Retirement

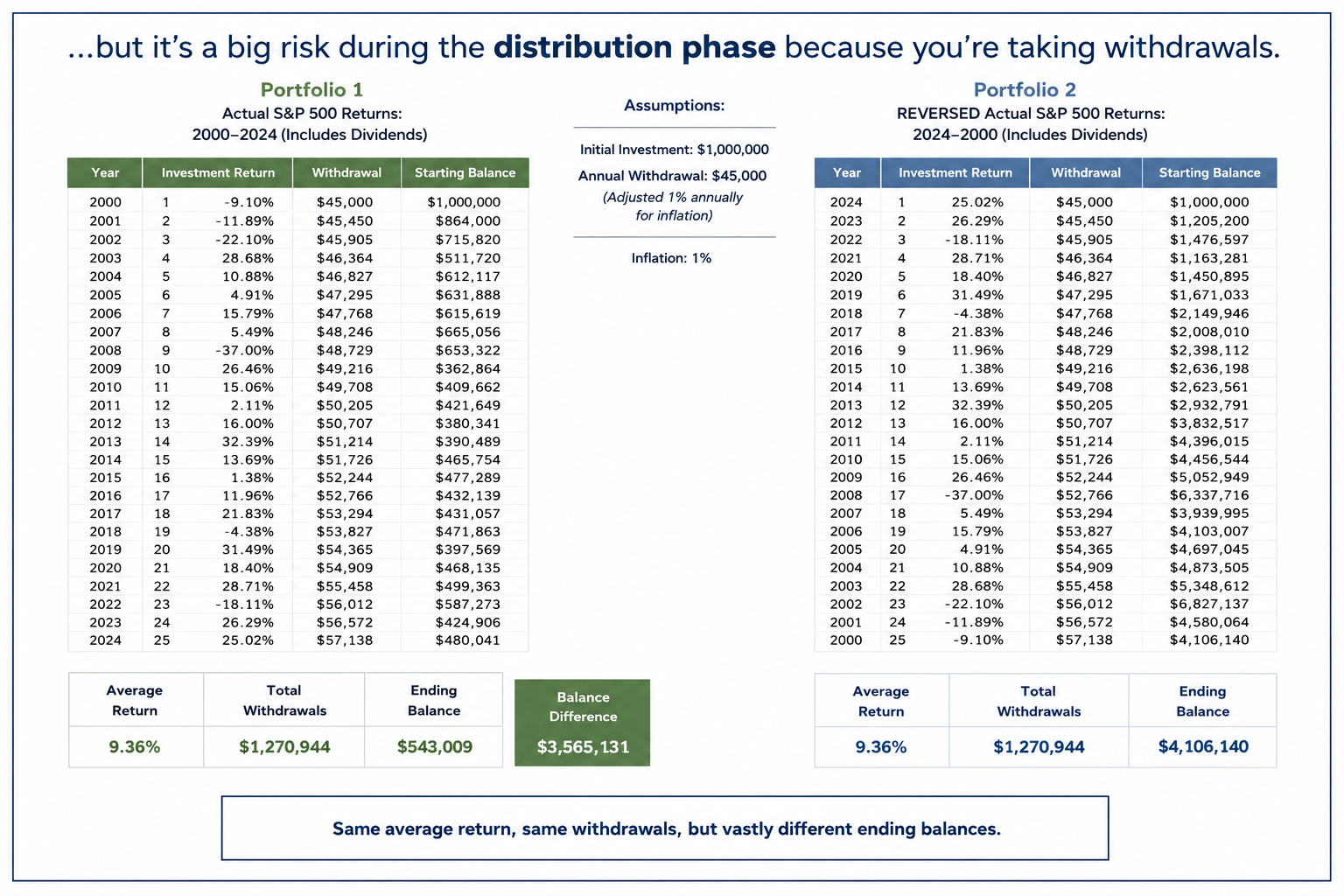

During retirement, market declines can have a larger impact when withdrawals are happening at the same time.

Even portfolios with similar long-term average returns may experience very different outcomes depending on the sequence in which returns occur. In some cases, two portfolios with the same average return can end with significantly different balances simply because the timing of positive and negative returns happened in a different order.

That’s why retirement income planning often involves more than investment performance alone. It also includes withdrawal strategy, cash flow planning, and managing risk over time.

Coordinating Retirement Income

Retirement income often comes from more than one source.

A thoughtful plan helps bring those pieces together into a strategy designed to support your lifestyle, adapt to changing needs, and provide greater clarity over time.

Whether income comes from Social Security, retirement accounts, pensions, investments, or cash reserves, the goal is to create a coordinated approach—not rely on any one source alone.

Our role is to help clients evaluate how these income sources may work together while considering taxes, market conditions, healthcare costs, and long-term goals.

Planning for Healthcare Costs

Healthcare expenses can become a larger part of retirement over time and they’re often one of the least predictable aspects of a long-term financial plan.

From Medicare decisions to out-of-pocket expenses and potential long-term care needs, planning ahead may help create greater clarity and reduce financial stress later in retirement.

A thoughtful retirement strategy considers how healthcare costs may fit into your broader income, savings, and legacy goals over time.

Planning for a Longer Retirement

Retirement today may last 25–30 years or longer, which can create new planning considerations beyond simply leaving the workforce.

A sustainable retirement strategy should account for ongoing income needs, inflation, healthcare costs, market volatility, and changing lifestyle goals over time.

The objective is to help create a plan designed not only for the early years of retirement, but for the decades that may follow.